Inflation in Brazil

an application of Time Series and Recurrent Neural Networks

Keywords:

IPCA, Monetary Policy, Box & Jenkins, SARIMA, LSTMAbstract

The realization of inflation forecasts is essential when one wants to improve strategic planning in order to reduce uncertainties and increase the planning capacity of families, companies and government, and thus ensure the proper functioning of the country's economy. Because of this, the objective of this study was to make forecasts of the Extended National Consumer Price Index (IPCA), which is the official metric for measuring inflation by the federal government. The Box and Jenkins and recurrent neural network techniques were used to build models that capture the information contained in the series, in order to evaluate the behavior of the variable analyzed over time, as well as to make predictions of future values. By applying the Box and Jenkins model, a SARIMA-type forecasting model was adopted, which considers both the trend and the seasonality in the series, being selected the one with the smallest mean square error (RMSE) and the smallest number of parameters. For the models of recurrent neural networks, the LSTM algorithm was used, and the one with the lowest RMSE was selected. In order to compare the two forecasting techniques, the criteria adopted were root mean square error (RMSE), and the SARIMA model proved to be the best model for predicting 12 direct months of inflation, while for short-term forecasts with feedback , the LSTM technique proved to be very effective.

References

ARESTIS, P.; PAULA, L.F.; FILHO, F.F. A nova política monetária: uma análise do regime de metas de inflação no Brasil. Economia e Sociedade, v 18, n. 1, p. 1-30, 2009.

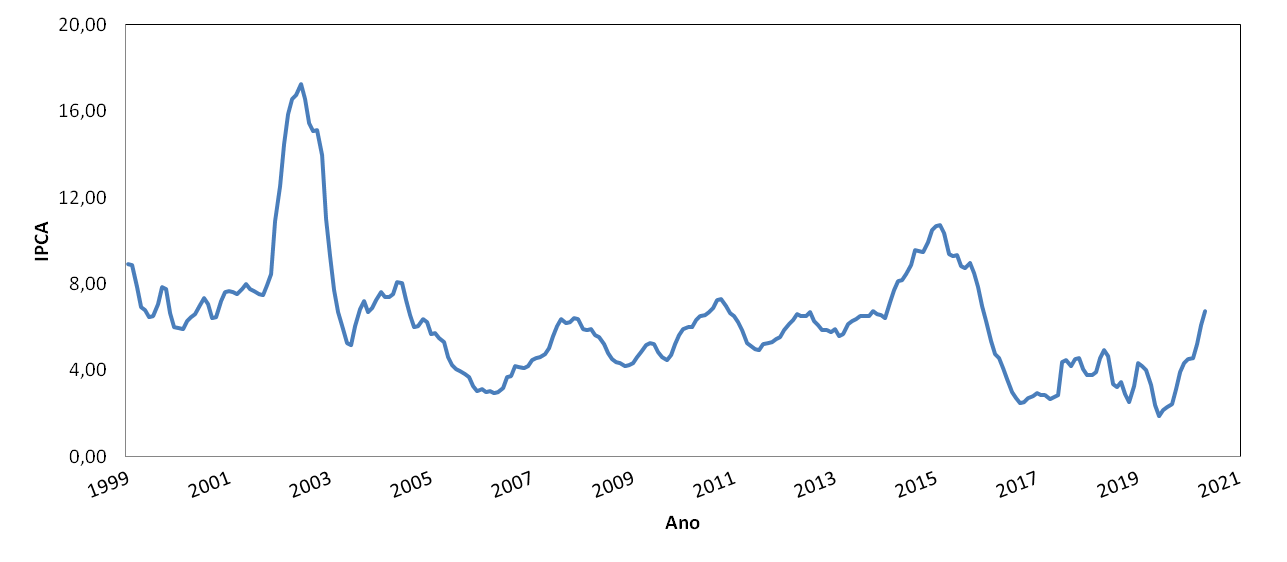

BACEN. Banco Central do Brasil, 2021. Disponível em: https://www.bcb.gov.br/.

BARBOSA, L.M. Prevendo a Inflação Brasileira: Comparação Entre um Modelo Teórico e um Ateórico de Séries Temporais. Boletim Informações Fipe, p. 44-49, 2019.

BONNO, S.J.P. Previsão de Inflação Utilizando Modelos de Séries Temporais. Dissertação de Mestrado, 2014.

BROWNLEE, J. Machine Learning Mastery, 2021. Disponível em: https://machinelearningmastery.com/category/lstm/.

BOX, G.E.P.; JENKINS, G.M.; REINSEL, G.C. Time Series Analysis: Forecasting and Control, v1, Wiley, 5$^a$ ed., 2015.

CAMARGO, D.; MOURA, R.F.S. Um Estudo Das Séries Temporais Dos Principais Indicadores Inflacionários Brasileiros E Seus Reflexos Na Performance Do Índice Ibovespa. SocArXiv, 2022. Disponível em: https://doi.org/10.31235/osf.io/x5w9v.

COLABORATORY, G. Google Colaboratory, 2021. Disponível em: https://research.google.com/colaboratory/

DAMETTO, R. C. Estudo da aplicação de redes neurais artificiais para predição de séries temporais financeiras. Dissertação de Mestrado, 2018.

FOUNDATION, T. D. LibreOffice Calc., 2021. Disponível em: https://www.libreoffice.org/discover/calc/.

IBGE, Instituto Brasileiro de Geografia e Estatística, 2021. Disponível em: https://www.ibge.gov.br/.

MARTELLI, O.P. Modelos LSTM para predição do preço da soja com base em dados climáticos brasileiros. 2021, 39p., Monografia- Universidade Tecnológica Federal do Paraná, Pato Branco.

MENDONÇA, H.F. Mecanismos de transmissão monetária e a determinação da taxa de juros: uma aplicação da regra de Taylor ao caso brasileiro. Economia e Sociedade, v.10, n.1, p.65-81, 2016.

MORETTIN, P.A.; TOLOI, C.M. Análise de Séries Temporais. São Paulo, Blucher, 2006.

OMS. Organização Mundial de Saúde, 2021. Disponível em: https://www.who.int/es.

PYTHON. Python Software Foundation, 2021. Disponível em: https://www.python.org/.

SIDRA, Sistema IBGE de Recuperação Automática - SIDRA, 2021, Disponível em: https://sidra.ibge.gov.br/.

R CORE TEAM. R: A Language and Environment for Statistical Computing, 2021. Disponível em: https://www.R-project.org/.

ZANIOL, C.; PAZINATTO, C.; SCHILLER, A.P.S.; MORAES, J.C.P. Previsão de inflação com o uso de Inteligência Artificial. Revista Brasileira de Computação Aplicada, v. 13, n. 2, p. 96–104, 2021.

Downloads

Published

How to Cite

Issue

Section

License

Proposta de Política para Periódicos de Acesso Livre

Autores que publicam nesta revista concordam com os seguintes termos:

- Autores mantém os direitos autorais e concedem à revista o direito de primeira publicação, com o trabalho simultaneamente licenciado sob a Licença Creative Commons Attribution que permite o compartilhamento do trabalho com reconhecimento da autoria e publicação inicial nesta revista.

- Autores têm autorização para assumir contratos adicionais separadamente, para distribuição não-exclusiva da versão do trabalho publicada nesta revista (ex.: publicar em repositório institucional ou como capítulo de livro), com reconhecimento de autoria e publicação inicial nesta revista.

- Autores têm permissão e são estimulados a publicar e distribuir seu trabalho online (ex.: em repositórios institucionais ou na sua página pessoal) a qualquer ponto antes ou durante o processo editorial, já que isso pode gerar alterações produtivas, bem como aumentar o impacto e a citação do trabalho publicado (Veja O Efeito do Acesso Livre).